영상 브리핑 · 약 12분. 데이터와 사실만으로 세 질문(측정·속도·귀속)을 연다.Video briefing · ~12 min. Opening three questions — measurement, speed, attribution — from data alone.

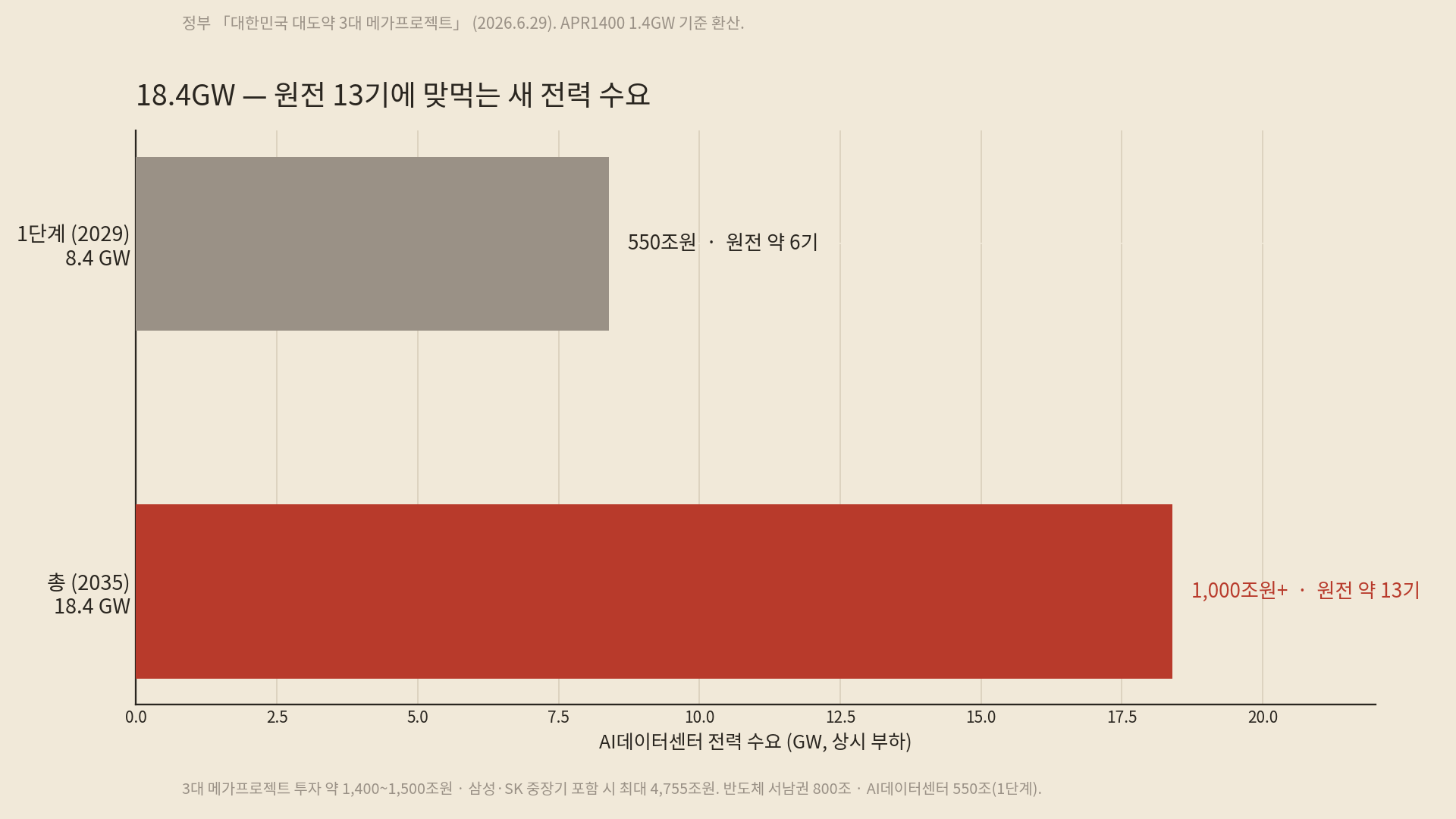

2026년 6월 29일, 청와대 영빈관. 정부는 반도체·피지컬AI·AI데이터센터를 묶어 「대한민국 대도약 3대 메가프로젝트」를 발표했다. 세 분야를 합친 투자 규모만 약 1,400조~1,500조원, 삼성·SK의 중장기 계획까지 더하면 최대 4,755조원에 이른다. 그중 AI데이터센터만 1단계로 8.4GW에 550조원이 들어가고, 2035년까지 18.4GW로 확장하면 1,000조원을 넘는다.

On June 29, 2026, at the Blue House state guest house, the government unveiled the "Three Mega-Projects for Korea's Great Leap Forward," bundling semiconductors, physical AI, and AI data centers. The combined investment in the three fields alone runs to roughly 1,400–1,500 trillion won; add the mid- and long-term plans of Samsung and SK, and the figure reaches up to 4,755 trillion won. Of that, the AI data centers alone take 550 trillion won for a first phase of 8.4 GW, passing 1,000 trillion won once expanded to 18.4 GW by 2035.

이 숫자의 무게를 실감하려면 전력으로 환산하면 된다. 데이터센터는 바람이 불든 안 불든 24시간 돌아가는 상시 부하다. 18.4GW는 대형 원전 약 열세 기에 맞먹는 새 수요다. 1단계 8.4GW만 해도 원전 여섯 기 몫이다. 반도체 생산기지도, 매년 쏟아질 AI 로봇도, 이 데이터센터도, 결국 전기 위에 선다.

To feel the weight of these numbers, convert them into power. A data center is a constant load that runs 24 hours a day whether the wind blows or not. 18.4 GW is new demand equivalent to about thirteen large nuclear reactors. The 8.4 GW first phase alone is worth six. The semiconductor bases, the AI robots to be rolled out year after year, these data centers — all of them, in the end, stand on electricity.

정부 스스로 그렇게 말했다. 이번 프로젝트를 "AI 대전환·에너지 대전환·국토 대전환을 동시에 추진하는" 것이라 규정했다. 순서를 눈여겨볼 것. 에너지가 빠지면 나머지가 서지 않는다. 전력 대책으로 2030년까지 재생에너지 100GW 조기 달성, 원전·SMR·ESS 병행, AI데이터센터 전용 전기요금제까지 내걸었다. 에너지 없이는 이 그림 전체가 무너진다 — 정부가 먼저 인정한 셈이다.

The government said as much itself. It defined the project as "advancing an AI transition, an energy transition, and a national-land transition all at once." Note the order. Take energy out, and the rest cannot stand. As its power measures, it pledged to reach 100 GW of renewables ahead of schedule by 2030, to run nuclear, SMRs, and ESS in parallel, and even to introduce a dedicated electricity tariff for AI data centers. Without energy, the whole picture collapses — the government conceded this first.

그렇다면 질문이 남는다. 우리는 그 전기를 얼마나 갖고 있으며, 얼마나 제대로 쓰고 있는가. 답의 한 조각이 뜻밖의 자료에 있다. 우리가 매년 버리는 깨끗한 전기의 기록이다.

Which leaves a question. How much of that electricity do we actually have, and how well are we using it? A piece of the answer sits in an unexpected place: the record of the clean electricity we throw away every year.

멈춰 세운 발전, 숫자로 보기

The generation we shut off, in numbers

출력제어(curtailment)란 발전할 수 있는데도 계통이 감당하지 못해 발전소의 출력을 강제로 줄이거나 멈추는 것을 말한다. 수요는 낮은데 재생에너지 발전이 한꺼번에 몰리는 봄·가을이면, 멀쩡히 만들 수 있는 전기를 만들지 않는다. 말 그대로 허공에 흘려보낸다.

Curtailment means forcibly reducing or halting a plant's output — even though it could generate — because the grid cannot absorb it. In spring and autumn, when demand is low but renewable output pours in all at once, we simply do not make electricity we could have made. We pour it, quite literally, into thin air.

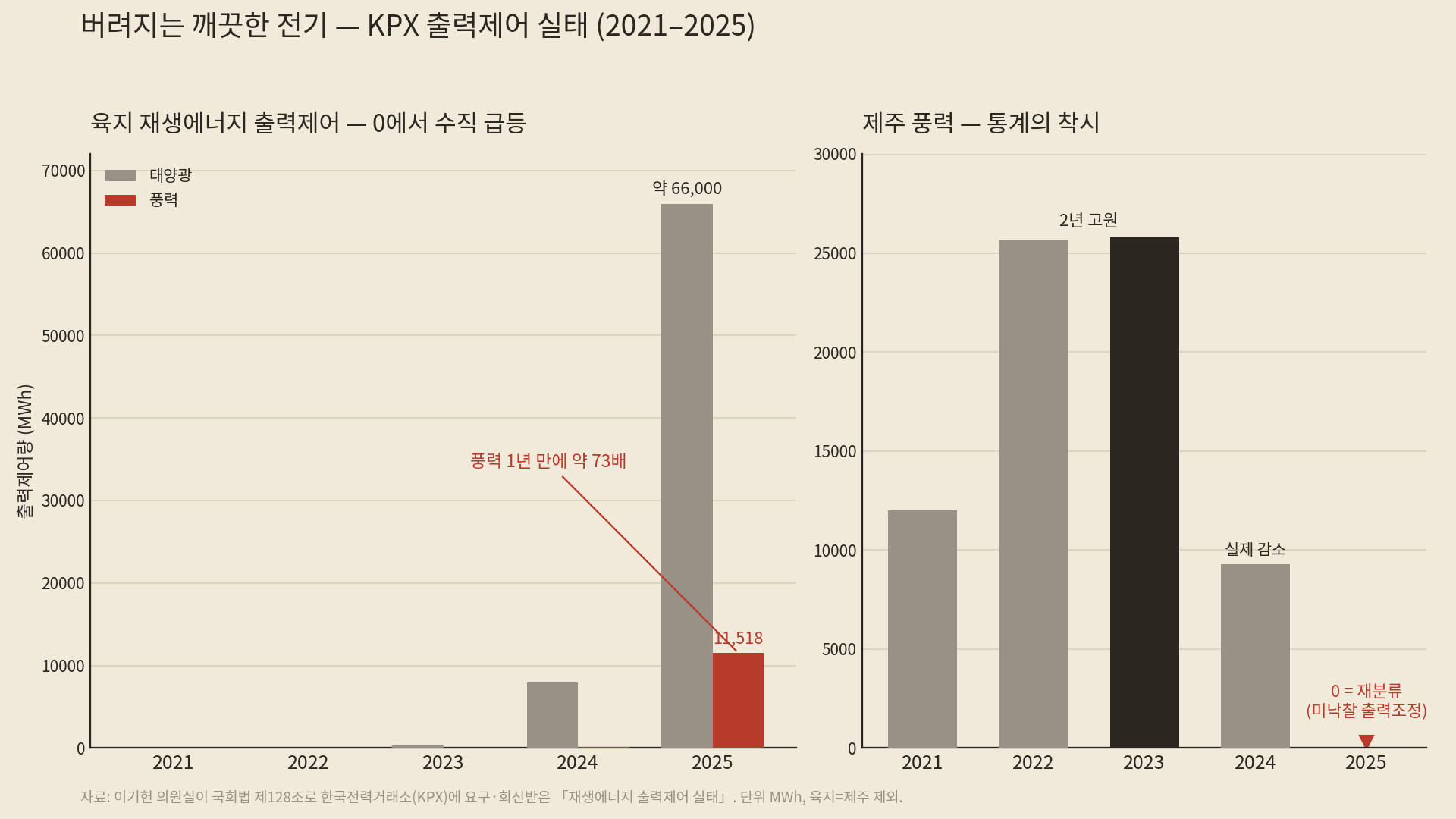

한국전력거래소(KPX) 자료를 이기헌 의원실이 국회법 제128조에 따라 요구해 받았다. 2021년 1월부터 2026년 5월까지, 월별 원자료다. 육지(제주 제외) 풍력만 뽑으면 추세가 선명하다.

Representative Lee Ki-heon's office obtained data from the Korea Power Exchange (KPX) under Article 128 of the National Assembly Act — monthly raw data from January 2021 to May 2026. Pull out onshore (excluding Jeju) wind alone, and the trend is stark.

| 연도 | 육지 풍력 출력제어 | 강원 | 호남 | 영남 |

|---|---|---|---|---|

| 2021~2023 | 사실상 0 | 0 | 0 | 0 |

| 2024 | 157 MWh | 34 | 122 | 1 |

| 2025 | 11,518 MWh | 3,262 | 5,043 | 3,213 |

단위 MWh · KPX 제공 수치

| Year | Onshore wind curtailment | Gangwon | Honam | Yeongnam |

|---|---|---|---|---|

| 2021–2023 | ~0 | 0 | 0 | 0 |

| 2024 | 157 MWh | 34 | 122 | 1 |

| 2025 | 11,518 MWh | 3,262 | 5,043 | 3,213 |

Unit: MWh · figures provided by KPX

육지 풍력 출력제어는 2023년까지 거의 0이었다. 2024년에 처음 의미 있게 나타났고, 2025년 한 해에 약 73배로 뛰었다. 강원만 보면 34에서 3,262로, 1년 만에 96배다.

Onshore wind curtailment was near zero through 2023. It appeared meaningfully for the first time in 2024, then jumped about 73-fold in a single year in 2025. In Gangwon alone, it climbed from 34 to 3,262 — 96-fold in one year.

정직하게 두 가지를 함께 말해야 한다. 하나, 절대량은 아직 작다. 전체 발전량에 견주면 미미하다. 둘, 그러나 추세가 이야기다. 0이던 곡선이 막 꺾여 올라가기 시작했다. 태양광은 더 크다. 2025년 육지 태양광 출력제어는 약 66,000 MWh에 이른다. 그중 호남이 40,723 MWh로 압도적이다. 충청은 사실상 0에서 11,786 MWh로 새로 튀어 올라 영남을 넘어섰다. 전선이 한 지역에 머물지 않고 번진다는 뜻이다.

Two things must be said honestly, together. One: the absolute volume is still small, negligible against total generation. Two: but the trend is the story. A curve that sat at zero has just bent sharply upward. Solar is larger still. In 2025, onshore solar curtailment reached about 66,000 MWh — Honam overwhelmingly dominant at 40,723 MWh, and Chungcheong surging from effectively zero to 11,786 MWh, overtaking Yeongnam. The front is not staying in one region; it is spreading.

원인도 데이터가 가리킨다. 2025년 육지 풍력 제어량은 4개 분기 중 2분기(봄)에 7,730 MWh로 압도적으로 쏠렸다. 봄철 공급과잉 — 수요는 낮은데 발전이 몰리는 수급 불균형 — 이 주된 원인이라는 것을, 계절 분포가 그대로 보여준다. 지금은 작아서가 아니라, 작을 때 들여다봐야 하는 문제다. 왜냐하면 재생에너지 100GW를 향해 가는 나라에서 이 곡선은 더 가팔라질 수밖에 없기 때문이다.

The cause, too, is written in the data. Of the 2025 onshore wind curtailment, 7,730 MWh — the largest share of the four quarters — fell in the second quarter (spring). Spring oversupply, the mismatch of low demand and concentrated generation, is the main driver, and the seasonal distribution shows it plainly. This is a problem to examine not because it is large, but while it is small — because in a country heading toward 100 GW of renewables, this curve can only steepen.

첫 번째 빈칸 — 손실은 누구의 몫인가

The first blank — whose loss is it?

여기서 자료의 가장 묵직한 대목이 나온다. 계통 안정을 위해 출력을 줄일 때, KPX는 중앙급전기든 재생에너지든 감발 그 자체에 대한 직접 보상은 없다고 밝혔다. 흔히 "중앙급전기는 감발 대가로 정산금을 받고 재생에너지는 못 받는다"고 요약되지만, KPX 원문은 그렇게 말하지 않는다. 감발 자체엔 어느 쪽도 직접 보상이 없다.

Here comes the heaviest passage in the data. When output is cut to keep the grid stable, KPX states that neither central-dispatch generators nor renewables receive any direct compensation for the curtailment itself. It is often summarized as "central-dispatch plants get paid for cutting output and renewables do not," but the KPX source does not say that. For the act of curtailment, direct compensation is absent on both sides.

진짜 비대칭은 다른 곳에 있다. 석탄·LNG·원자력 같은 중앙급전기는 거래소의 급전지시를 이행하는 대가로 용량정산금(CP) 등을 받는 시장 구조 안에 있다. 반면 재생에너지 같은 비중앙급전기는 그 구조 밖에 있어, 멈춰도 기댈 정산 틀이 아예 없다. 차이는 "감발을 보상받느냐"가 아니라 "CP 구조 안이냐 밖이냐"다. 재생에너지가 우선 구매 등 정책적 지원과 계통 기여에 대한 별도 정산을 받긴 하나, 못 판 전기의 기회손실은 온전히 발전사 몫으로 남는다.

The real asymmetry lies elsewhere. Central-dispatch plants — coal, LNG, nuclear — sit inside a market structure that pays them capacity payments (CP) and the like in return for following the exchange's dispatch orders. Renewables, as non-central-dispatch generators, sit outside that structure, with no settlement framework to fall back on when they stop. The difference is not "whether curtailment is compensated" but "inside or outside the CP structure." Renewables do receive priority purchase and separate settlement for grid contribution, yet the opportunity loss of the power they could not sell falls entirely on the generator.

KPX도 이 불균형을 인정한다. 자료에서 거래소는 「재생e 입찰제」를 대안으로 검토 중이라고 밝혔다. 재생에너지도 중앙급전기와 유사하게 전력시장 입찰에 참여하고 CP를 받게 하는 방식이다. 보상의 빈칸을 시장으로 메우려는 시도다. 옳은 방향일 수 있다. 그런데 바로 그 입찰제가, 제주에서 통계의 함정을 만든 장본인이다.

KPX acknowledges the imbalance. In the data, the exchange states it is reviewing a "renewable bidding scheme" as an alternative — a scheme in which renewables, like central-dispatch generators, enter market bidding and receive CP. It is an attempt to fill the compensation blank through the market. It may well be the right direction. And yet that very bidding scheme is what created the statistical trap in Jeju.

측정의 함정 — 제주가 보여준 것

The measurement trap — what Jeju revealed

제주는 육지보다 먼저, 더 크게 겪었다. 풍력 출력제어량이 2023년 약 25,800 MWh에 달했다. 그런데 2025년 제주 풍력 출력제어는 0으로 떨어진다.

Jeju felt it earlier and harder than the mainland. Its wind curtailment reached about 25,800 MWh in 2023. And yet in 2025, Jeju's wind curtailment falls to zero.

문제가 풀려서가 아니다. 제주가 2024년 6월 재생에너지 입찰제도를 도입한 뒤, 이전에 "출력제어"로 잡히던 것의 상당 부분이 "미낙찰로 인한 출력조정"으로 분류가 바뀌었기 때문이다. KPX 자료의 각주가 이를 직접 밝힌다 — 제주는 입찰제도 시행 후 미낙찰 출력조정 외의 출력제어는 없다고. 발전사가 시장에서 낙찰받지 못해 발전을 못 하는 것은 형식상 출력제어가 아니므로, 통계에서 사라진다.

Not because the problem was solved. After Jeju introduced the renewable bidding scheme in June 2024, much of what had been recorded as "curtailment" was reclassified as "output adjustment due to non-award." A footnote in the KPX data says so directly: after the bidding scheme took effect, Jeju has no curtailment other than output adjustment from non-award. A generator failing to win in the market and therefore not generating is, formally, not curtailment — so it disappears from the statistics.

더 정밀하게 보면 두 단계다. 제주 풍력은 2022·2023년 약 25,600~25,800 MWh로 2년간 고원을 이뤘다. 그러다 2024년 9,265 MWh로 실제로 먼저 줄었다. 그리고 2025년, 통계상 0으로 사라졌다. 앞의 감소는 진짜다. 뒤의 0은 재분류다.

Look more precisely and there are two stages. Jeju's wind curtailment formed a plateau of about 25,600–25,800 MWh across 2022–2023, then actually fell first to 9,265 MWh in 2024, and vanished to a statistical zero in 2025. The former decline is real. The latter zero is reclassification.

입찰제도의 공을 깎을 생각은 없다. 그것은 진짜 개선을 담고 있다. 낙찰된 재생에너지는 SMP에 더해 용량정산금 등 일반 발전기와 동등한 정산을 받고, 감발 시 기대이익정산금이 열린다. "멈추라 해놓고 보상은 0"이라던 빈칸을 시장 메커니즘으로 메우는 방향이 맞다. 실시간·예비력 시장과 VPP가 과공급에 유연하게 대처할 제도적 기반도 깐다. 여기까지는 재분류가 아니라 실질이다.

There is no intent to diminish the bidding scheme's merit. It carries genuine improvement. Awarded renewables receive settlement on par with conventional plants — SMP plus capacity payments — and an expected-profit settlement opens when they are curtailed. Filling the "ordered to stop, paid nothing" blank through a market mechanism is the right move. Real-time and reserve markets, together with VPPs, also lay the institutional groundwork for flexibly handling oversupply. To this point it is substance, not reclassification.

문제는 입찰제도가 배분·가격 장치이지 수요 창출 장치가 아니라는 데 있다. 봄·가을 과공급이라는 물리적 사실 — 그 순간 계통이 감당 못 하는 잉여 — 은 그대로다. 바뀌는 것은 "누가, 어떤 가격에 멈추느냐"이지 "잉여가 사라지느냐"가 아니다. 제주에서도 가격원리에 따라 여전히 제어가 일어난다. 다만 그것이 "출력제어" 칸에서 "미낙찰 출력조정" 칸으로 옮겨 적히면서, 통계상 0이 된 것이다. 물리적 낭비는 사라진 게 아니라 눈에서 사라졌다.

The problem is that the bidding scheme is an allocation-and-pricing device, not a demand-creation device. The physical fact of spring–autumn oversupply — the surplus the grid cannot absorb in that moment — is unchanged. What changes is "who stops, and at what price," not "whether the surplus disappears." In Jeju, curtailment by price merit-order still occurs. It is simply moved from the "curtailment" column to the "non-award output adjustment" column, and so becomes a statistical zero. The physical waste has not vanished; it has vanished from view.

측정이 바뀐 것과 문제가 풀린 것은 다르다. 입찰제가 육지로 확대되면 "출력제어량"이라는 숫자는 줄어들 수 있다. 그러나 남아도는 깨끗한 전기 자체가 사라지는 것은 아니다. 제도를 평가할 때, 우리가 보는 지표가 현실을 가리키는지 아니면 회계의 칸 이동을 가리키는지 구분해야 한다.

A change in measurement is not the same as a solution to the problem. If the bidding scheme expands to the mainland, the number called "curtailment" may shrink. But the surplus clean electricity itself does not disappear. When evaluating a policy, we must distinguish whether the indicator we watch points to a lifted physical constraint or merely to a shift between accounting columns.

이미 시작된 대응 — 그리고 남는 것

The response already underway — and what remains

그렇다면 남는 전기를 무엇으로 바꿀 것인가. 이 질문에 정부가 손 놓고 있는 것은 아니다. 오히려 이미 폭넓게 움직인다. 가장 큰 축은 분산에너지 특화지역(분산특구)이다. 2025년 6월 전력 직접거래 고시가 시행됐고, 11월에는 전남·제주·부산·경기(의왕) 네 곳이 첫 지정됐다. 전력시장을 거치지 않고 사업자가 사용자에게 직접 전기를 파는 "지산지소" 구조다. 발상은 정확히 "버려질 잉여를 그 자리에서 흡수한다"이다 — 출력제어가 잦은 전남 태양광 밀집지에 데이터센터를 유치해 지역 안에서 생산하고 소비하겠다는 것이 대표 사례다. 지정된 네 곳 모두 ESS를 핵심 모델로 내세웠다. 여기에 잉여전력을 열로 바꾸는 P2H, 수소로 바꾸는 그린수소 수전해(P2G), 전기차 배터리를 계통 자원으로 쓰는 V2G, 그리고 서해안·U자형 에너지고속도로까지 이미 판 위에 있다.

So what will we turn the surplus into? The government is not standing idle. If anything, it is already moving broadly. The largest axis is the Distributed Energy Special Zones. The direct-power-trade notice took effect in June 2025, and in November four sites — South Jeolla, Jeju, Busan, and Gyeonggi (Uiwang) — were designated first. It is a "local production, local consumption" structure in which operators sell electricity directly to users without going through the power market. The idea is precisely "absorb the surplus where it is wasted" — the flagship case being to attract data centers to South Jeolla's solar-dense, curtailment-heavy areas so power is generated and consumed within the region. All four designated sites put ESS forward as a core model. Add P2H (turning surplus power into heat), green-hydrogen electrolysis (P2G), V2G (using EV batteries as a grid resource), and the West Coast and U-shaped energy highways, and much is already on the board.

그러니 자강헌은 "대안은 유연한 수요와 저장이다"라고 뒤늦게 말하려는 것이 아니다. 그건 정부가 이미 정책 규모로 하고 있다. 우리가 물으려는 것은 다른 것이다. 이미 추진되는 대안들이, 정말로 물리적 낭비를 줄이는가. 그리고 바로 여기서, 방금 발표된 메가프로젝트가 문제를 다시 날카롭게 만든다.

So Jaganghean is not belatedly declaring that "the alternative is flexible demand and storage." The government is already doing that at policy scale. What we mean to ask is different: do the alternatives already underway actually reduce the physical waste? And here is exactly where the just-announced mega-project sharpens the problem again.

18.4GW의 AI데이터센터는, 간헐적 재생에너지로 채우기 가장 어려운 종류의 수요다. 데이터센터는 바람이 멎었다고 멈출 수 없는 24시간 상시·고신뢰 부하다. 재생에너지와 짝지으려면 잉여를 "그냥 쓰는" 것으로는 안 되고, 막대한 저장과 백업이 필요하다. 정부가 재생에너지 옆에 원전·SMR·ESS를 나란히 붙인 이유가 그것이다. 즉 "버릴 전기를 데이터센터가 흡수하면 된다"는 서사는 절반만 참이다. 멈춰도 되는 일(학습)에는 맞지만, 멈출 수 없는 일(추론·서비스)에는 맞지 않는다.

18.4 GW of AI data centers is the hardest kind of demand to fill with intermittent renewables. A data center is a 24-hour, high-reliability constant load that cannot pause because the wind died down. To pair it with renewables, "just using" the surplus is not enough; it requires enormous storage and backup. That is exactly why the government placed nuclear, SMRs, and ESS right alongside renewables. In other words, the narrative that "data centers will absorb the electricity we would throw away" is only half true. It fits work that can pause (training), but not work that cannot (inference and service).

가장 예민한 부하 — 반도체 팹

The most sensitive load — the semiconductor fab

그런데 데이터센터보다 한 단계 더 극단인 부하가 있다. 반도체 팹이다. 데이터센터는 전력이 끊겨야 멈춘다. 팹은 전력이 미세하게 흔들리기만 해도 손실이 난다. 3대 메가프로젝트의 반도체 축 — 서남권 800조, 충청 156조 — 이 모두 이 예민한 부하 위에 선다.

But there is a load one step more extreme than a data center: the semiconductor fab. A data center stops only when power is cut. A fab takes a loss when power merely wavers. The semiconductor axis of the mega-project — 800 trillion won in the southwest, 156 trillion in Chungcheong — all stands on this exquisitely sensitive load.

첫째는 진동이다. EUV 노광장비는 웨이퍼와 마스크를 나노미터·나노초 단위로 정렬한다. 둘은 서로 반대 방향으로 5G·15G로 가속한다. 그러면서도 단 한 번의 진동도 내지 않아야 한다. 팹이 진동을 극단적으로 억제한 기초 위에 세워지는 이유다. 지반이 진동을 얼마나 붙잡아 주느냐가 수율의 사활을 가른다.

The first issue is vibration. An EUV lithography tool aligns wafer and reticle to the nanometer and nanosecond. The two accelerate in opposite directions at 5 g and 15 g. And they must do so without a single vibration. That is why a fab is built on a foundation engineered to suppress vibration to an extreme. How well the ground holds that vibration decides the fate of yield.

둘째는 전력 품질이다. 팹은 어떤 산업 부하보다 엄격한 전기를 요구한다. 밀리초 단위의 순간전압강하 하나가 공정 중인 웨이퍼를 파괴한다. 사고 한 번에 수백만 달러가 날아간다. 그래서 업계엔 SEMI F47이라는 전용 규격이 있다. 팹은 UPS·ESS·발전기를 겹겹이 깔아 계통의 흔들림으로부터 스스로를 격리한다.

The second is power quality. A fab demands cleaner electricity than any other industrial load. A single millisecond-scale voltage sag can destroy a wafer mid-process. One such incident can cost millions of dollars. That is why the industry keeps a dedicated standard, SEMI F47. Fabs layer UPS, ESS, and generators to isolate themselves from the grid's tremors.

여기서 출력제어와 한 줄로 이어진다. 재생에너지가 늘수록 계통의 변동은 커진다. 데이터센터가 못 견디는 그 변동을, 팹은 더더욱 못 견딘다. 그러니 "간헐적으로 생산되는 전기"의 문제는 양이 아니다. 얼마나 공급하느냐가 아니라, 얼마나 안정적이냐다. 그리고 국가가 대도약을 거는 가장 값진 부하들이 — 팹과 데이터센터가 — 바로 그 불안정에 가장 취약하다.

Here it connects, in one line, back to curtailment. The more renewables on the grid, the greater its variability. The variability a data center cannot endure, a fab endures even less. So the problem with "intermittently generated electricity" is not quantity. It is not how much is supplied, but how stable it is. And the most valuable loads the nation is staking its great leap on — the fab and the data center — are precisely the least tolerant of that instability.

남는 세 개의 질문

The three questions that remain

버려지는 것과 굶주리는 것이 같은 계통 위에 동시에 존재한다. 한쪽 끝에서 우리는 깨끗한 전기를, 그걸 쓸 수요가 그 시간·그 자리에 없어서 버린다. 다른 쪽 끝에서 국가는 원전 열세 기에 맞먹는 수요를 세운다. 둘을 잇는 다리는 하나 — 발전과 수요를 시간과 장소에서 맞추는 것. 그 다리를 놓는 일이 쉽지 않다는 것을, 지금까지의 자료가 말한다. 그래서 진짜 질문은 세 가지로 모인다.

The wasted and the starving exist at once, on the same grid. At one end we throw away clean electricity because there is no demand for it in that time and place. At the other, the nation erects demand equivalent to thirteen nuclear reactors. The bridge between them is one thing — matching generation and demand across time and place. That the bridge is hard to build is what the data has been telling us. So the real questions converge on three.

첫째, 측정. 우리가 성과라 부르는 지표가 물리적 낭비의 감소인가, 아니면 회계 칸의 이동인가. 제주의 0이 그 경계를 이미 흐려 놓았다.

First, measurement. Is the indicator we call an achievement a reduction in physical waste, or a shift between accounting columns? Jeju's zero has already blurred that line.

둘째, 속도. 에너지 대전환의 속도가 18.4GW라는 수요의 속도를 따라잡는가. 데이터센터 착공은 2028년, 재생에너지 100GW는 2030년, 에너지고속도로는 그 뒤다. 수요는 지금 세워지고, 잉여는 지금 자란다. 그 시차를 무엇이 메우는가 — 혹시 그 사이 화석연료를 더 태우게 되는가.

Second, speed. Does the pace of the energy transition catch up with the pace of 18.4 GW of demand? Data-center construction begins in 2028, 100 GW of renewables in 2030, the energy highway after that. Demand is being erected now; the surplus is growing now. What fills that gap — and might we burn more fossil fuel in the meantime?

셋째, 귀속. 그렇게 세워지는 에너지 대전환이 결국 누구의 것이 되는가. 버려지는 깨끗한 전기는 여러 지역, 여러 발전사에서 나온다. 그 전기를 삼킬 거대한 수요와 그 위에 서는 산업은 누구의 손에 모이는가. 답을 파는 자리에서가 아니라, 이 질문을 정직하게 여는 자리에서 자강헌은 말한다.

Third, attribution. Whose does the energy transition, built this way, ultimately become? The wasted clean electricity comes from many regions and many generators. Into whose hands do the vast demand that will swallow that power, and the industry that stands upon it, converge? Not from the seat of one who sells answers, but from the seat of one who honestly opens this question, Jaganghean speaks.

깨끗한 전기를 허공에 버린다는 것은, 결국 우리가 가진 에너지 주권의 일부를 버린다는 뜻이다. 자강헌이 'Active Neutrality'를 이야기해온 이유도 여기에 있다. 자원과 기술을 남의 손에 의존하지 않으려면, 먼저 우리 손에 이미 있는 것을 흘려보내지 않아야 한다. 국가의 대도약이 에너지 위에 서 있다고 정부가 선언한 바로 그 순간, 우리는 그 에너지를 — 아직 작지만 가파르게 — 버리고 있다. 작은 숫자가 가파르게 자라는 지금이, 그 답을 설계하기에 가장 좋은 때다.

To pour clean electricity into thin air is, in the end, to throw away part of the energy sovereignty we hold. This is why Jaganghean has spoken of "Active Neutrality." To avoid leaning on others' hands for resources and technology, we must first stop letting slip what is already in our own. At the very moment the government declared that the nation's great leap stands on energy, we are throwing that energy away — still small, but steepening. Precisely now, while the small number climbs steeply, is the best time to design the answer.

자료 출처

Sources

재생에너지 출력제어 수치는 이기헌 의원실이 국회법 제128조에 따라 한국전력거래소(KPX)에 요구해 받은 「재생에너지 출력제어 실태」 자료(2026년 6월 회신)이며, 육지·제주 및 권역별 구분은 원자료 분류를 따랐다. 3대 메가프로젝트 수치는 산업통상부 「대한민국 대도약 3대 메가프로젝트 국민보고회」(2026년 6월 29일) 발표에 근거한다. 분산에너지 특화지역 지정은 2025년 11월 정부 발표에 따른다. 출력제어 근거법령: 전기사업법 제27조의2·제45조, 분산에너지 활성화 특별법 제16조.

Renewable curtailment figures are from the "Renewable Energy Curtailment Status" data obtained by Rep. Lee Ki-heon's office from the Korea Power Exchange (KPX) under Article 128 of the National Assembly Act (received June 2026); onshore/Jeju and regional breakdowns follow the original data's classification. Mega-project figures are based on the Ministry of Trade, Industry and Energy's "National Report on Korea's Great Leap Three Mega-Projects" (June 29, 2026). Distributed Energy Special Zone designations follow the government's November 2025 announcement. Legal basis for curtailment: Electric Utility Act Arts. 27-2 and 45; Distributed Energy Activation Special Act Art. 16.