워싱턴의 한 사람이 168달러를 나눠 갚기로 했다. 사치품이 아니었다. 칫솔, 욕실 세제, 그리고 운동 보조제. 일자리를 잃은 뒤, 비싼 카드빚을 더하지 않으려고 'Buy Now, Pay Later'로 생필품을 쪼갠 것이다. 그는 말한다. 자기는 오늘 당장 운동화를 원하는 무책임한 사람이 아니라고. 석사 학위가 둘이고, 한때 10만 달러 넘게 벌었다고. 그래도 충분하지 않을 수 있다고.

A man in Washington decided to pay off $168 in installments. Not on luxuries — a toothbrush, bathroom cleaner, a tub of pre-workout. After losing his job, he split the cost of daily necessities through Buy Now, Pay Later, rather than add expensive credit-card debt. He is not, he says, some irresponsible person chasing sneakers today. He holds two master's degrees; he once earned over six figures. And it still may not be enough.

자강헌은 흔히 한 줄로 자신을 정의한다. 흔들리는 시대에 도박판으로 떠밀리는 사람이 자기 발로 설 기반을 스스로 세우도록 돕는 곳. 위 장면은 그 정의의 살(肉)이다. 떠밀리는 자리가 미국에도 있고, 그 떠밀림은 칫솔의 형태로 온다.

Jagangheon often defines itself in a single line: a place that helps those shoved toward the rigged game in a shaking age build the ground to stand on their own feet. The scene above is that definition made flesh. The place of being shoved exists in America too — and the shove arrives in the shape of a toothbrush.

사슬을 본다

Seeing the Chain

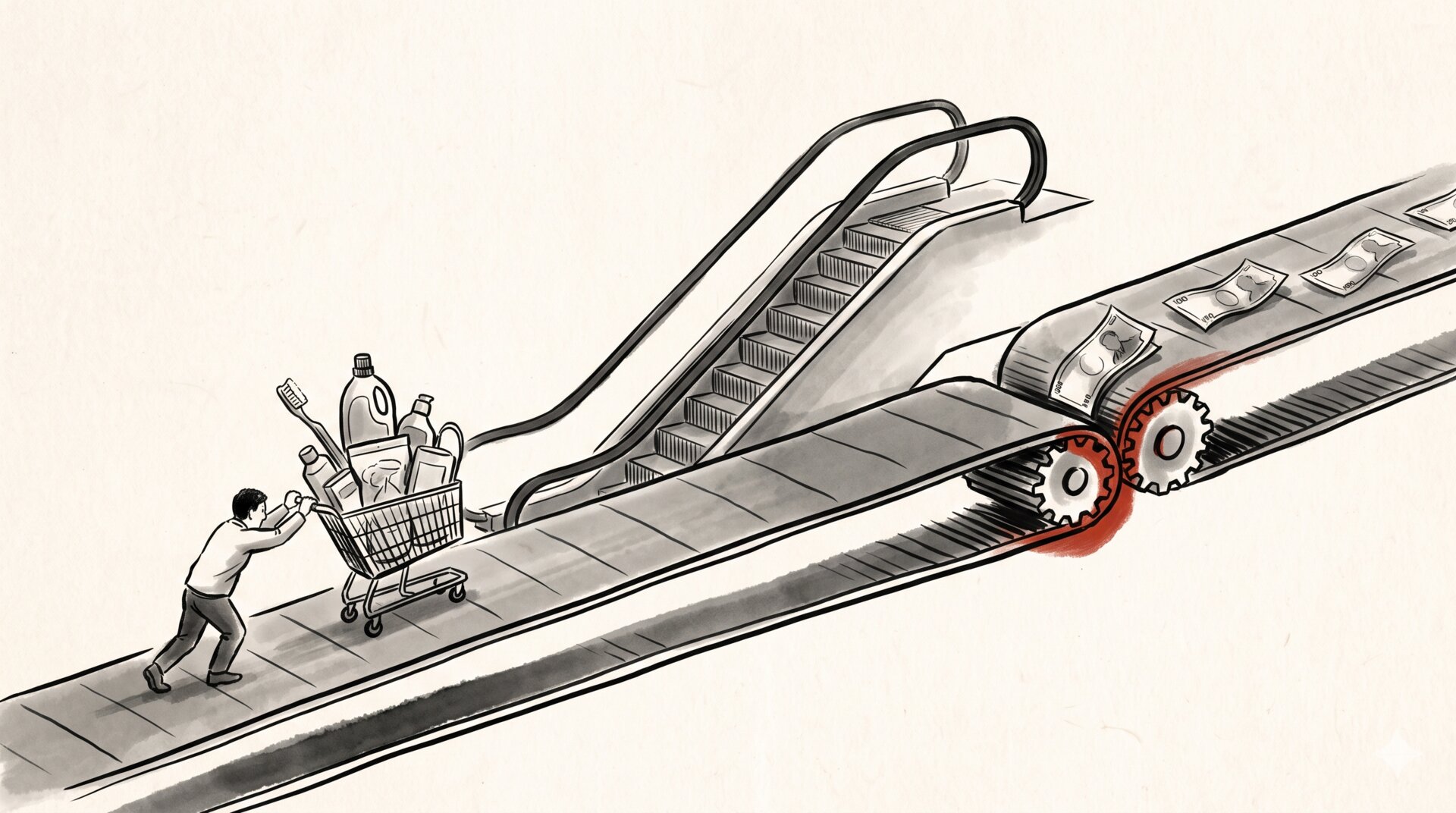

겉으로 BNPL은 소비자와 가맹점 사이의 일이다. 그러나 그 뒤에는 더 긴 사슬이 있다. 사모신용이라 불리는, 월스트리트의 추적 바깥에서 움직이는 자본 — Blue Owl, KKR, Elliott — 이 'forward-flow'라는 계약으로, 아직 만들어지지도 않은 대출을 미리 사들인다. 소비자 자산이 다른 곳보다 더 벌어 줄 것이라는 베팅이다.

On the surface, BNPL is a matter between a consumer and a merchant. But behind it runs a longer chain. Private credit — capital that moves beyond Wall Street's usual tracking, names like Blue Owl, KKR, Elliott — agrees, through "forward-flow" arrangements, to pre-purchase loans before they are even made. It is a bet that consumer assets will out-earn the alternatives.

이 구조의 효과는 단순하다. 대출을 만든 쪽(Klarna, Affirm, PayPal)은 위험을 즉시 장부에서 털어내고, 수수료를 챙기고, 다시 대출할 자본을 푼다. 그리고 더 많이 찍어낼 동기를 얻는다. 회의론자들은 서브프라임 모기지의 평행을 본다 — 위험과 보상이 분리되면, 만드는 쪽은 질이 아니라 양을 좇는다.

The effect is simple. The party that originates the loan — Klarna, Affirm, PayPal — clears the risk off its books at once, collects fees, and frees capital to lend again. And it gains an incentive to churn out more. Skeptics see the parallel to subprime: when risk is detached from reward, the originator chases volume, not quality.

더 깊은 문제는 보이지 않는다는 것이다. 일부 BNPL은 단기 할부 데이터를 신용평가기관에 넘기지 않는다. 그래서 차주의 진짜 건강 상태는 측정되지 않는다. 'phantom debt' — 유령 부채. 그리고 Moody's가 짚는 핵심: 이 forward-flow 모델은 오늘의 규모로는 경기 하강에서 시험된 적이 없다.

The deeper problem is that it cannot be seen. Some BNPL platforms withhold short-term installment data from the credit bureaus, so the true health of the borrower goes unmeasured. Phantom debt. And the point Moody's presses: at today's scale, this forward-flow model has never been tested in a downturn.

두 함성을 사지 않는다

Buying Neither Shout

기사 안에는 두 목소리가 있다. 하나는 "서브프라임의 재현"이라 외치고, 다른 하나는 "사전 검증된 소비자에게, originator도 일부를 보유하니 규율된다"고 답한다. 능동적 중립은 어느 함성도 사지 않는다. 공포도, 안심도 상품이다.

The reporting holds two voices. One cries "subprime, again." The other answers that the loans target pre-vetted consumers, and that originators retain a slice, so discipline holds. Active Neutrality buys neither shout. Fear is a product; reassurance is a product.

대신 구조를 본다. 질문은 "사기인가 아닌가"가 아니다. 질문은 이것이다 — 호황에는 보이지 않다가, 하강에서 가장 약한 끝단부터 끊기는 사슬인가. 그렇다면 이름이 무엇이든, 그것은 도박판이다.

It looks instead at the structure. The question is not "fraud or not." The question is this: is it a chain invisible in the boom that snaps at its weakest end in the downturn? If so, then whatever its name, it is a rigged game.

과거는 서막이다

What Is Past Is Prologue

한국인은 이 기계를 안다. 우리는 그것을 이미 겪었다.

Koreans know this machine. We have already lived it.

2003년, 카드대란. IMF 위기 직후, 정부는 경기를 부양하고 탈세를 막으려 신용카드 사용을 적극적으로 밀었다. 규제가 풀리자 카드사들은 상환능력이 검증되지 않은 사람들에게까지 카드를 던졌다 — 서명만 한 고등학생에게도. 2002년, 1억 장이 넘는 카드가 거리를 돌았고, 사람들은 한 카드의 빚을 다른 카드로 막았다. 돌려막기. 그 고리가 끊기는 순간, 파산이 시작됐다.

2003: the card crisis. In the wake of the IMF shock, the government aggressively pushed credit-card use — to revive consumption and to curb tax evasion. As regulation loosened, issuers threw cards even at people whose ability to repay was never verified — at high-schoolers who merely signed. By 2002, more than 100 million cards circulated, and people covered one card's debt with another. Rolling it over. The moment that loop broke, the bankruptcies began.

숫자는 차갑다. 2003년 신용불량자 372만 명 중 239만 명, 60퍼센트가 카드 관련이었다. 카드사들의 자기자본비율은 13퍼센트에서 마이너스 5.4퍼센트로 무너졌다. 업계 1위 LG카드가 채권단으로 넘어갔다. 그리고 숫자 바깥에는, 숫자로 적을 수 없는 비용이 있었다 — 무너진 가계, 깨진 가정.

The numbers are cold. Of 3.72 million people in default in 2003, 2.39 million — over 60 percent — were card-related. Issuers' capital ratios collapsed from 13 percent to minus 5.4. LG Card, the industry's largest, was handed to its creditors. And beyond the numbers lay a cost no number records — households broken, families undone.

같은 기계다. 부양 신용이 검증되지 않은 손에 흘러들고, 그 신용이 생활 그 자체를 메우고(그때는 돌려막기, 지금은 쪼개진 칫솔), 위험이 가려지고(그때는 돌려막기의 위장, 지금은 유령 부채), 만드는 쪽이 위험에서 분리되고, 그리고 — 하강에서 시험된다.

It is the same machine. Stimulus credit flowing into unverified hands; that credit filling life itself (rolling-over then, a split toothbrush now); risk concealed (the disguise of rolling-over then, phantom debt now); the originator detached from the risk; and then — tested in the downturn.

신용카드와 BNPL은 같은 빚이 아니다

A Credit Card and BNPL Are Not the Same Debt

그러나 거울은 차이도 비춰야 한다. 게으른 유비는 자강헌의 것이 아니다. 2003년의 기계는 신용카드였고, 오늘의 기계는 BNPL이다. 둘은 같은 빚이 아니다.

But a mirror must reflect difference too. Lazy analogy is not Jagangheon's. The machine of 2003 was the credit card; today's machine is BNPL. They are not the same debt.

| 차원 | 신용카드 (2003 카드대란의 기계) | BNPL (오늘의 기계) |

|---|---|---|

| 구조 | 개방형 회전 신용, 이자 부과 | 폐쇄형, 4회 분할, 무이자(즉시 보유) |

| 유저 | 광범위, 회전 잔액 | 점점 한계 소비자, 생필품 연명(설문 54% "생존 필수") |

| 금융사·위험 소재 | 카드사가 채권 보유(보유 목적) — 위험 집중 | 핀테크가 즉시 매각(발행 후 분산) — 사모신용으로 위험 분산·은닉 |

| 가시성 | 신용평가기관에 보고됨 | Pay-in-4 상당수 미보고 → 유령 부채 |

| 규제 | TILA(진실대출법) 전면 적용 | TILA 대체로 비적용; 적용하려던 2024년 규칙은 2025년 철회 |

| 위기 양상 | 카드사의 직접 붕괴(LG카드) | 어디 떨어지는지 보이지 않는 분산형 |

| Dimension | Credit card (the 2003 machine) | BNPL (today's machine) |

|---|---|---|

| Structure | Open-end revolving credit, interest-bearing | Closed-end, four installments, interest-free |

| User | Broad, revolving balances | Increasingly marginal consumers, necessities as lifeline (54% call it a survival need) |

| Originator & where risk sits | Issuer holds the receivables — concentrated | Fintech offloads at once — risk dispersed into private credit, concealed |

| Visibility | Reported to credit bureaus | Much of Pay-in-4 unreported → phantom debt |

| Regulation | Fully under TILA | Largely outside TILA; the 2024 rule that would have applied it was withdrawn in 2025 |

| Failure mode | Direct collapse of the issuer (LG Card) | Dispersed — where it lands cannot be seen |

가장 깊은 차이는 위험이 어디 앉느냐다. 카드대란에서 카드사는 채권을 직접 들고 있었다 — 그래서 차주가 무너지면 카드사가 함께 무너졌다. 집중된 붕괴. BNPL은 시작과 동시에 위험을 사모신용으로 잘게 흩는다. 개별 핀테크의 파산 위험은 낮아지지만, 그 위험이 어느 펀드의, 누구의 포트폴리오에 숨었는지 추적이 끊긴다. 카드대란은 'LG카드'라는 이름으로 무너졌다. BNPL의 붕괴에는 이름이 없을지 모른다.

The deepest difference is where the risk sits. In the card crisis, issuers held the receivables themselves — so when borrowers fell, the issuers fell with them. A concentrated collapse. BNPL disperses the risk into private credit from the start. The bankruptcy risk of any single fintech falls, but the trail to where that risk hides — in whose fund, in whose portfolio — is cut. The card crisis fell under a name: LG Card. BNPL's collapse may have no name.

그리고 규모. 카드대란은 신용불량자 수백만의 거시 위기였다. 오늘의 BNPL은 빠르되 아직 그 무게는 아니다 — 다만 사모자본과의 융합이 그 뇌관을 키운다.

And scale. The card crisis was a macro event of millions in default. Today's BNPL is fast but not yet that weight — though its fusion with private capital keeps swelling the fuse.

제동의 방향

The Direction of the Brake

가장 날카로운 차이는 제동에 있다. 한국은 위기 뒤 국가가 브레이크를 밟았다. 여신전문금융업법을 고쳐 현금대출 잔액이 신용판매 잔액을 넘지 못하게 묶고, 길거리 모집을 금지했다. 미국은 지금 반대로 간다.

The sharpest difference is the brake. After its crisis, Korea's state pressed the pedal: it rewrote the law so cash-advance balances could not exceed credit-sale balances, and it banned street solicitation. America, now, goes the other way.

2024년 5월, 연방소비자금융보호국(CFPB)은 BNPL의 디지털 계정을 신용카드로 보고, 분쟁·환불 같은 진실대출법(TILA)의 보호를 BNPL에 적용하려는 해석규칙을 냈다. 그러나 1년 뒤인 2025년 5월, 권한대행 국장 러셀 보트(Russell Vought)는 그 규칙을 예순일곱 개의 다른 지침과 함께 거둬들였다. 그리고 다시 내지 않겠다고 했다. BNPL을 신용카드처럼 들여다보려던 연방의 한 시도가, 그렇게 1년 만에 접혔다.

In May 2024, the Consumer Financial Protection Bureau (CFPB) issued an interpretive rule treating BNPL's digital accounts as credit cards — extending Truth in Lending protections like dispute and refund rights to BNPL. But a year later, in May 2025, acting director Russell Vought withdrew that rule along with sixty-seven other guidance documents. And said it would not be reissued. A federal attempt to look at BNPL as a credit card was folded, just a year on.

브레이크에서 손을 뗀 것이다. 다만 그 손길이 한 방향만은 아니다 — 같은 시기 뉴욕주는 거꾸로, BNPL 사업자에게 라이선스와 실체적 제한을 부과하는 법에 서명했다. 연방이 페달에서 발을 떼는 동안, 일부 주는 페달을 밟는다. 이 어긋남 자체가, BNPL에 내장된 폭발력을 가리키는 규제의 징후다.

The foot came off the brake. But not in one direction only — in the same period, New York went the opposite way, signing a law imposing licensing and substantive limits on BNPL providers. As the federal pedal lifts, some states press down. That very divergence is a regulatory sign of the explosive force built into the BNPL model.

그리고 한국

And Korea

우리는 그 기계를 부순 적이 있다. 문제는, 같은 기계가 다시 조립되는 신호를 지금 어디서 보는가이다.

We have broken this machine before. The question is where, now, we see it being reassembled.

카드대란 이후 금융감독원은 위험의 신호를 명명했다 — 유동성 경색, 연체율 급등, 현금서비스 증가. 오늘의 판본으로 번역하면: 사모신용의 위축, BNPL 연체의 상승, 그리고 생필품이 빚으로 넘어가는 비율. 청년의 부채, 리볼빙, 빚으로 산 베팅. 이름은 새것이되, 동사는 같다.

After the card crisis, the financial regulator named the warning signs — liquidity strain, surging delinquency, rising cash advances. Translated into today's version: private credit pulling back, BNPL delinquency climbing, and the share of necessities crossing over into debt. Youth debt, revolving balances, bets bought on borrowed money. The names are new; the verb is the same.

자강헌은 추상적 강령에서 출발하지 않는다. 우리는 본다. 그리고 본다는 것은, 칫솔 한 자루가 빚이 되는 순간을 사슬 전체로 읽어내는 일이다.

Jagangheon does not begin from abstract doctrine. We see. And to see is to read the moment a single toothbrush becomes debt as one whole chain.

코다: 이 읽기가 맞다면, 그 증거는 다음 하강에서 온다 — 사모신용이 발을 빼고, BNPL의 자금줄이 가늘어지고, 가장 약한 끝단의 소비자가 가장 먼저 끊길 때. 우리는 그날을 기다려 채점할 것이다. 함성을 사지 않고, 구조를 적어두고.

Coda: if this reading is right, its proof will come in the next downturn — when private credit pulls its foot back, when BNPL's funding thins, and when the consumer at the weakest end is cut off first. We will wait for that day to mark the score. Buying no shout, and writing down the structure.